Understanding how credit cards operate is, ironically, both simple and difficult at the same time. They are quite simple to utilize because of the convenience they provide. To finish your transaction, all you need is one swipe. Understanding how the credit card interest rate is applied to your purchases, on the other hand, can be a difficult nut to crack. People are perplexed by it. As a result, a credit card can be both a blessing and a curse. If you don't want to bring cash with you, a single credit card will enough. You can go shopping and then pay it off later. However, if you have a rewards card, it's an even better offer! You can earn points, receive incentives, or receive cash back while taking advantage of the many benefits of using credit cards. However, due to the interest rate levied by credit card companies, paying off your credit card debt may take a little longer if you have a balance.

Credit card interest rates, also known as finance charges, are determined by the credit card provider. Aside from that, the interest rate varies depending on the card you have from the same issuer. As a result, interest rates are a large part of the credit card's bright picture, and one must be informed of the interest rate that applies to their card and how it is computed. Thus in this blog we will help you in understanding how does the computation of Credit Card Interest works.

Credit Card Interest: Meaning

Every purchase you make with your credit card incurs an interest rate known as the Annual Percentage Rate (APR). It is the cost charged by the credit card company for allowing you to borrow money to spend. This interest is calculated on the amount you owe each month at the end of the month. If you have a balance on your account, you will be charged extra fees. Some credit cards, on the other hand, carry a variable rate of interest that fluctuates with the prime rate. As a result, make sure to read the tiny print attentively. The credit card rate will rise if the prime rate rises. It's worth noting that if you pay your credit card payments in full and on time, you won't be charged anything. In the UAE, interest rates on credit cards are only applied if you are late with a payment or have an outstanding balance. So there's no reason to be hesitant about getting a credit card in the United Arab Emirates.

What is the mechanism behind it?

APR, or annual percentage rate, is the rate of interest levied on your credit card transactions at the end of each month, as stated in the bill. The daily rate is used by the credit card company to calculate the interest rate on your account. This daily rate is calculated by dividing your interest rate by the number of days in a year, which are 365. The corporation then multiplies this daily figure by your amount at the conclusion of each day for the duration of a billing cycle. For example, a consumer in the UAE might spend AED 1000 on items with their credit card.

This sum, however, is not squandered in a single day. It is rather spent in installments over the course of a month. As a result, the card's net balance will fluctuate depending on the amount spent. This is a perplexing procedure. So, the average daily balance, or ADB, is calculated by dividing the total amount owing to the company by the number of days in the month.

The ADB can be determined mathematically using the formula below:

ADB= The supplied balance multiplied by the number of days carried forward / the number of days in the month. Every transaction is charged with the ABD, and at the end of the month, all of the daily balance scores are added together to determine the ultimate rate of interest paid on any credit card in the UAE.

How can I lower the Interest Rate on my Credit Card?

Some of the criteria that determine your credit card's interest rate are within your control. With a higher credit score, you'll have more credit card alternatives. If your credit score has dramatically improved, you may be able to negotiate a reduced rate with the provider. However, regardless of the listed APR on your card, there are various ways to lower the effective rate:

MAKE A COMPLETE PAYMENT ON YOUR CREDIT CARD BALANCE

Between the purchase date and the payment due date, most credit card companies provide you at least a 21-day grace period. You won't be charged interest on new purchases made during this period if you pay off your balance in full and don't have any outstanding cash advances.

INVEST A LITTLE MORE THAN THE BARE MINIMUM

If you can't pay off your entire balance, pay off as much as you can to avoid late fees and lower your overall interest-bearing total. Typically, the minimum payment is up to 3% of the outstanding total. Any amount you pay above this minimum will cut your interest charges even more.

How can you figure out what a good credit card interest rate is?

It might be tough to determine what constitutes a reasonable rate of interest for clients to consider when applying for a credit card. The interest rate you pay will be determined by several factors, including the credit card business and your credit score. Those with a good credit score might get the best interest rates since the lenders feel there is less risk involved. On the other hand, customers with a poor credit score or no credit history would have a difficult time obtaining lower interest rates. When compared to persons with a solid credit history, they frequently qualify for high interest rates, sometimes nearly double. As a result, make sure to keep a decent credit score in order to benefit from lower rates.

What is the difference between an interest rate and an annual percentage rate (APR)?

Although the terms "interest rate" and "annual percentage rate" are frequently used interchangeably, they are distinct ideas in some situations. The APR, or annual percentage rate, for mortgages, automobile loans, and other types of installment loans includes both interest and extra charges such as points and fees. As a result, your mortgage interest rate and annual percentage rate (APR) will differ slightly.

When it comes to credit cards and other types of revolving credit accounts, however, the two phrases are interchangeable. Your APR does not include any additional credit card fees, such as annual fees and late fees.

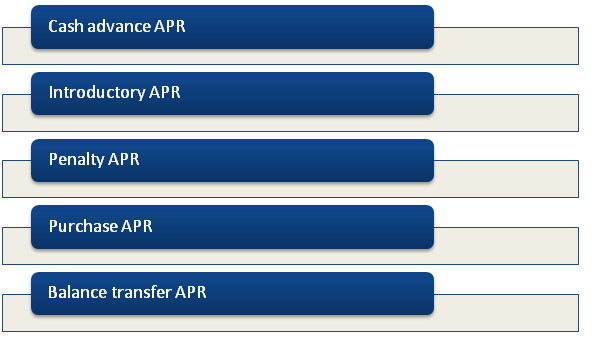

What are the different types of Interest Rates and Annual Percentage Rate?

There are various distinct sorts of APRs on credit cards that you should be aware of.

CASH ADVANCE APR

The interest rate that is charged on the money borrowed from your credit card. This is usually more expensive and does not provide a grace period. Many experts say that if you use your credit card to acquire a cash advance, you will start paying interest as soon as the transaction is completed.

INTRODUCTORY APR

Some credit card providers offer a special APR to entice you to sign up for their card. For a limited time, this can apply to purchases and/or debt transfers, and it's usually lower than the card's regular APR which is occasionally even 0%.

PENALTY APR

Interest will be levied if you make late payments or break any of the cards’s other terms and conditions. This is usually the highest APR, and it may be levied if your payments are more than 60 days late.

PURCHASE APR

The rate of interest charged on purchases made with the card.

BALANCE TRANSFER APR

The rate of interest charged on balance transfers from one credit card to another.

Conclusion

Having an outstanding credit card bill will cost you a lot of money. As a result, it's a good idea to stick to your payback schedule. However, don't allow the astronomically high interest rates frighten you away from acquiring a credit card. If you're still unsure, you can apply for a balance transfer card to relieve yourself of the worry of debt.