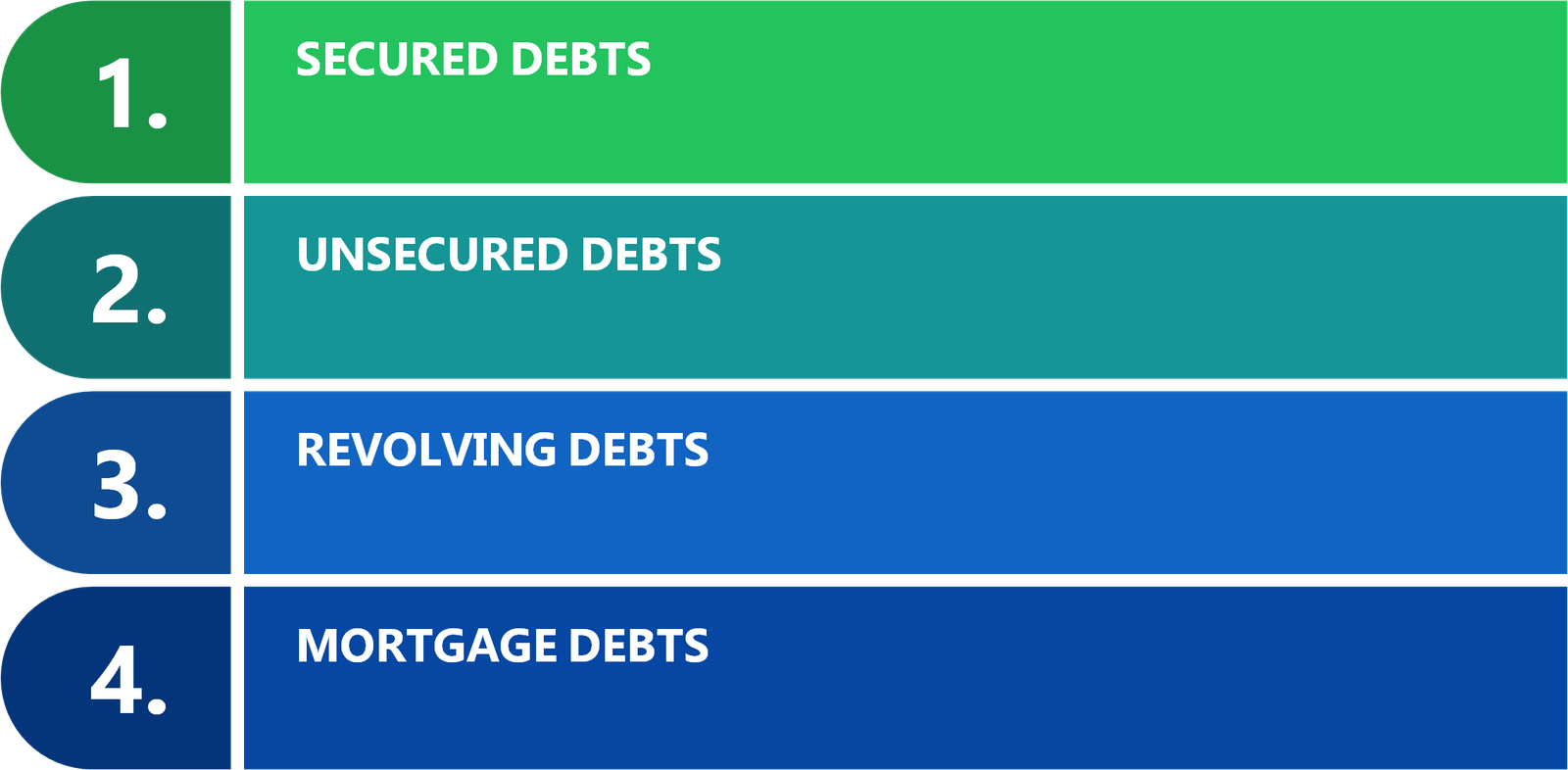

A debt is an amount owed to the owner for the usage of money that has not been paid back. Almost everyone has to deal with debt at some point in their lives. Not all debts are created equal, and some obligations are seen as more valuable than others. All debts can be classified into four categories:

- Secured Debt

- Unsecured debts

- Revolving debts

- Mortgage debts

Types of Debts in UAE Explained

SECURED DEBTS

A secured debt is one that is backed up by an asset as collateral. Before giving any loan to the borrower, the lender would usually check the borrower's payment history. A credit report will provide important details regarding a borrower's payment history. In secured debt, an asset is used as collateral to secure a loan.

For example, if a borrower has a strong credit score but fails to pay the obligation, the lender will acquire complete ownership of the asset. If the borrower fails to repay the loan, the collateral asset may be taken. The lender has the option to sell the asset and make a profit.

Secured debt needs collateral and is not based on the creditworthiness of the borrower. Secured assets are mortgage home loans with terms ranging from 15 to 30 years and a collateral asset as security.

For example, a loan with secured collateral of a car is given to a borrower. To buy an automobile, the lender provides cash. The car is placed under a lien, which implies that the issuer now owns the vehicle. A loan issuer will be the owner's name. If the borrower defaults on the car loan, the lender may sell the vehicle to recuperate payments. The interest rate on secured loans is rather reasonable.

UNSECURED DEBTS

Unsecured debt is a type of debt that is issued without the use of collateral. Without the asset as collateral, the lender makes a loan. A lender issues a loan to a borrower solely on the basis of the borrower's good faith, credit score, and ability to repay, and promise to return the debt.

Despite the lack of a guarantee or supporting security, the borrower has a contractual obligation to repay payments to the lender. If the borrower defaults for any reason, the lender has the right to pursue legal action to recoup the loan. For the lender, this procedure is dangerous, time-consuming, and costly. As a result, the interest rate on an unsecured loan is much higher than on a secured loan. Personal loans, credit cards, and other forms of unsecured debt are examples.

REVOLVING DEBTS

Revolving Debt is a loan agreement between a lender and a customer that allows the consumer to borrow money up to a particular maximum limit on a repeating basis. A credit card is the best illustration of revolving credit.

A credit card has a set limit, and the cardholder can spend as much as they want within that limit. The credit card issuing business determines the credit card amount limit and type of credit card.

Revolving debt is calculated using credit card fund amounts and monthly loan installments. Unsecured and secured debt, such as a home equity line of credit, can both constitute revolving debt.

MORTGAGE DEBTS

Mortgage debt is one of the largest and most prevalent loans that practically all borrowers have. Mortgage debt is a loan used to purchase an asset using collateral as a security and subject to specified terms. A home loan is a type of secured mortgage debt that is tied to the real estate industry.

Among consumer loans, mortgage debt has the lowest interest rate. To make properties affordable for customers, mortgage loans range from 15 to 30 years.

Tips to avoid Debt in UAE

We have explained the types of debts in UAE above, but it is up to you to not end up with anyone of them in future. Rest assured, our Experts have devised certain tips which you can follow to avoid being burdened with Debts in UAE.

Residents of the UAE are progressively putting themselves in debt by taking out personal loans or using credit cards. Individual debt levels in the UAE are the third highest in the region, according to the latest statistics. 46.7 percent of the population, or 4.3 million people, are in debt, with 12.8 percent actively seeking credit.

Lenders use a potential borrower's current Debt-Burden Ratio (DBR) when assessing their repayment ability and a DBR of close to or above 50% will instantly exclude you from future borrowing. Unfortunately, many of the country's debt-stricken debtors already have DBRs that are significantly in excess of this level.

Here are some tips to have a healthy banking lifestyle:

MAKE A BUDGET

Examine your financial statements more closely and create a monthly budget for yourself. Keep a financial log to track your income and expenses, and don't spend more than you earn. Keeping track of your records will assist you in better managing your funds and achieving your long-term financial objectives.

SAVE

Determine what lifestyle changes you should make to help you get out of debt. For example, a family with two automobiles could sell one and save money on insurance, fuel, and maintenance. Make a distinction between your "needs" and "wants," and keep your financial goals in mind.

START A SAVINGS ACCOUNT

Set aside a portion of your money in an account where you can earn interest. When unexpected circumstances arise, a savings account can also be used as an emergency fund.

INVESTMENTS

Leaving your money in a bank account generates no income. Instead, invest in little, low-cost items like gold or mutual bonds to help you build your financial portfolio.

DONOT FALL FOR ‘GET RICH QUICK’ SCHEMES

It takes time and effort to make a solid investment. Be wary of offers that promise fast and big profits in a short period of time. Learn how to spot "pyramid" and "networking" con artists. If something sounds too good to be true, it almost certainly isn't.

DEALS

Avoid buying things on the spur of the moment. Do the majority of your shopping at the Dubai Shopping Festival, and keep an eye out for bargains all year.

DEBT CONSOLIDATION

Combine all of your existing loans and credit card debt into one loan to benefit from reduced interest rates, longer repayment terms, and smaller monthly payments.

REGULATE DBR

The amount of debt payment deducted from your monthly wage is known as your DBR. The legal limit in the UAE is 50%, so if you earn AED10,000, make sure your debt repayments don't exceed AED5,000. You should aim for a DBR of 25-30% to accommodate for instances when you may require additional credit.

BE ADVISED

When it comes to deciding what to do with your money, financial literacy can help you make the best decisions. Consider attending a financial literacy or management programme, and if you want to invest in the stock market or any other sort of investment, don't be hesitant to call your bank and ask for professional guidance.

Conclusion

Surely no one wants to end up with Debts, but circumstances can lead us to it. With better planning and proper implementation you can be debt free to a great extent. We hope this blog provided you with incite full information. For more information on other related aspects, feel free to check out our Website as well.

DhanGuard: All-in-One Solution for Business Setup in Dubai, UAE

DhanGuard is your ultimate one-stop solution for all your business needs. Whether you’re planning to set up a new company or expand your existing business in the UAE, we’ve got you covered with our comprehensive range of services. From Company Formation in UAE and Business Bank Account in UAE services to managing your financial and legal compliance, we provide everything you need under one roof.

Our services include:

- Company Formation in UAE and Dubai

- Opening a Business Bank Account in UAE and Dubai with a 99% success rate

- VAT & Corporate Tax Compliance

- Accounting, Bookkeeping, and Auditing Services

- Trade License Renewal

- Golden Visa Assistance

Let DhanGuard make your journey of Business Setup in Dubai seamless and hassle-free!