Are you considering buying a home in the bustling city of Dubai or the advanced landscapes of the UAE? Several home loan products are available in the United Arab Emirates to meet the needs of various buyers. As a prospective buyer, you would want to shop around for the best deals appropriate for your long-term goals, but there are other factors to consider when applying for a UAE home loan. Buying a home is one of the most amazing acquisitions most people will ever make. It is crucial to understand everything there is to know about the property you are buying and whatever finance you are using to make it happen. In this blog, we explore the importance of having a co-applicant for your UAE home loan while shedding light on the possibilities of obtaining a home loan without one.

Who is a Co-Applicant?

A co-applicant joins the principal applicant or borrower in applying for a home loan. There is no legal requirement for a co-applicant, and lenders only need it if certain conditions are met. However, obtaining a co-applicant increases the likelihood of a loan application being accepted because the income of both borrowers is combined, making it easier to meet the eligibility requirements. Since their revenues are pooled, co-applicants can obtain a larger loan. However, it's worth noting that, in some instances, the co-applicant's income might not be considered when calculating the loan's income eligibility requirements.

What are the benefitsa of applying for a Home Loan with a Co-Applicant in the UAE?

Applying for a home loan with a co-applicant in the UAE can offer several benefits, depending on the applicant's financial situation and relationship.

Here are some of the advantages of having a co-applicant for a home loan in the UAE:

-

Higher Loan Eligibility

-

Lower Interest Rates

-

Improved Creditworthiness

-

Shared Financial Responsibility

-

Tax Benefits

-

Faster Loan Approval

-

Divided Repayment Burden

Who can apply as a Co-applicant for taking a Home Loan in UAE?

Who may be a co-applicant is governed by a set of laws. A minor cannot be a co-applicant because they cannot enter into a contract legally. Co-applicants are usually required to be spouses and blood relatives.

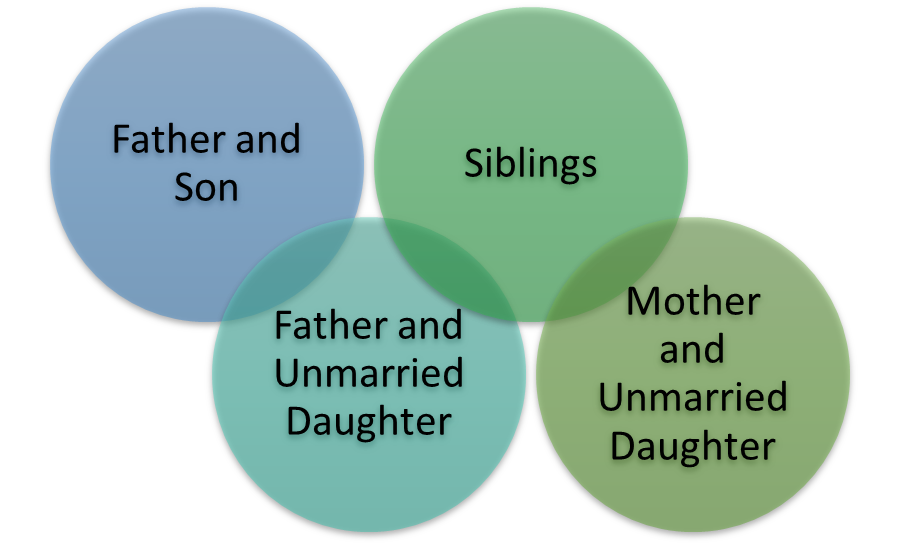

The following are examples of appropriate co-applicants:

Father and Son

The father and the son will apply for the loan if the son is an only child. Both applicants' salaries will be considered, the property will be in their names, and either will be the primary owner. The father cannot be the sole owner of the property if there are several sons and the father and son want to apply for a loan together.

Father and Unmarried Daughter

If a father and an unmarried daughter are co-applicants, the property must only be in the daughter's name. This prevents any potential legal issues following the daughter's marriage. The father's earnings are not taken into account.

Mother and Unmarried Daughter

The property is in the daughter's name, and the mother's income is not considered, just as it is in the case of a father-and-daughter combination.

Siblings

If two brothers live together and plan to do so in the new home, they will apply for a joint loan together. A few lenders may require both parties to be co-owners. On the other hand, a brother cannot apply for a loan with his sister.

What are the requirements for obtaining a home loan in the United Arab Emirates with a co-applicant?

Banks in the United Arab Emirates usually use four critical criteria to determine whether a person is eligible for a home loan with their co-applicant:

-

Time spent in the UAE (typically six months to a year)

-

The average work tenure in the United Arab Emirates is five years (typically a minimum of 6 months)

-

A trip to the United Arab Emirates on business (typically 2 to 3 years)

-

A credit history

Is a Co-Applicant Mandatory for Your Home Loan in the UAE?

The UAE is a rapidly growing real estate market, and the region's unique financial and cultural dynamics often guide its lending practices. While having a co-applicant is not always mandatory, it can significantly impact the approval and terms of your home loan.

Here are some key reasons why having a co-applicant can be beneficial:

Enhanced Creditworthiness:

Having a co-applicant with a strong financial background can bolster your combined creditworthiness, increasing the chances of loan approval.

Increased Loan Eligibility:

With a co-applicant, you can apply for a higher loan amount, which may be essential for purchasing your desired home.

Better Interest Rates:

Lenders may offer more favourable interest rates when there are multiple applicants, as it spreads the risk and ensures the loan's repayment.

Ease of Documentation:

When you share the responsibility with a co-applicant, the paperwork can become more manageable, streamlining the application process.

Sharing Financial Responsibility:

A co-applicant can share the financial responsibility of repaying the loan, which can be especially useful for joint family home purchases.

Home Loan Without a Co-Applicant

While having a co-applicant can be advantageous, it's not always necessary. If you're pursuing a home loan without one, here are some factors to consider:

-

Sufficient Income: You must have a stable and substantial income to qualify for a home loan without a co-applicant. Lenders will evaluate your income, financial stability, and ability to repay the loan independently.

-

Good Credit History: A strong credit history can compensate for the absence of a co-applicant. Ensure your credit report is in good shape, and make timely payments on your debts.

-

Down Payment: You may need to provide a larger down payment if you don't have a co-applicant. This demonstrates your commitment to the purchase.

-

Debt-to-income Ratio: Lenders will scrutinize your debt-to-income ratio, so managing your existing debts wisely is essential.

Exploring the Option of a Joint Home Loan with a Family Member

Many people opt for a joint home loan with a family member, often a sibling, to make homeownership more accessible. This arrangement offers several benefits:

-

Combined Income: By pooling your income, you can qualify for a larger loan amount, expanding your options in the competitive UAE real estate market.

-

Shared Repayment Responsibility: Both you and your co-applicant, like your brother, share the responsibility of repaying the loan, reducing the financial burden on each individual.

-

Better Credit Profile: A co-applicant with a strong credit history can offset any shortcomings in your financial profile.

-

Ease of Documentation: Joint home loans simplify the paperwork, as you and your co-applicant collaborate on the application and share the documentation requirements.

Conclusion

Abu Dhabi, the capital of the UAE, offers a diverse real estate market. The same principles apply if you're purchasing property in the heart of the city. A co-applicant can still enhance your chances of securing a home loan in Abu Dhabi, while going solo is also feasible, given the right financial circumstances.

In conclusion, while a co-applicant is only sometimes mandatory for a home loan in the UAE, their presence can significantly impact your home-buying journey. It's essential to carefully evaluate your financial situation and consider the benefits of having a co-applicant before deciding. Whether in Dubai or Abu Dhabi, the right choice can help you unlock the doors to your dream home in the UAE. Dhanguard will guide you at every step of your Home Loan journey. Contact us today!

DhanGuard: All-in-One Solution for Business Setup in Dubai, UAE

DhanGuard is your ultimate one-stop solution for all your business needs. Whether you’re planning to set up a new company or expand your existing business in the UAE, we’ve got you covered with our comprehensive range of services. From Company Formation in UAE and Business Bank Account in UAE services to managing your financial and legal compliance, we provide everything you need under one roof.

Our services include:

- Company Formation in UAE and Dubai

- Opening a Business Bank Account in UAE and Dubai with a 99% success rate

- VAT & Corporate Tax Compliance

- Accounting, Bookkeeping, and Auditing Services

- Trade License Renewal

- Golden Visa Assistance

Let DhanGuard make your journey of Business Setup in Dubai seamless and hassle-free!